Patience is no longer a common virtue in consumers of the modern-day payments ecosystem. Be it capital markets, financial institutions, retail consumers or millennials; everyone is looking for instantaneous results which are secure and frictionless. No wonder the real-time payments/instant payments market is witnessing accelerated growth globally.

As per Grand View Research, the global real-time payments market size was valued at US $17.57 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 35.5% from 2023 to 2030. The global real-time payments transactions volume was valued at over US $100 billion in 2022.

The future is real-time payments

India’s UPI has been a front-runner in instant payments, widely successful and acclaimed globally as one of the most efficient instant payment infrastructures. The growth in UPI volumes is up almost 100% YoY (year-on-year) in August 2022. Amounts transacted also grew by 75% YoY. We are talking about 6.5 billion transactions worth almost US $130 billion in a month!

The Federal Reserve in the US is developing the FedNow Service, due to launch in 2023, to create a new infrastructure to support 24x7x365 instant payments. This is bound to be a game changer for US payments industry, just like India’s UPI or Brazil’s Pix infrastructure.

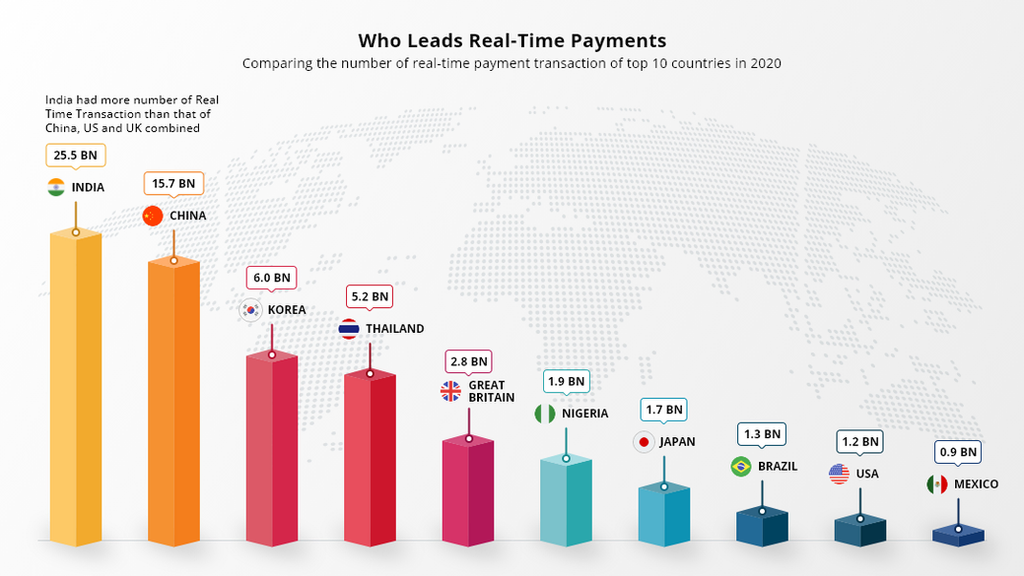

*Source: Economist Intelligence Unit, ACI Worldwide

How has the risk & fraud ecosystem innovated with real-time payments?

Common types of frauds that impact a real-time payment infrastructure are quite different from traditional financial crime. In many cases they exploit consumer naivety and lack of awareness.

- Phishing – Using spam emails to extract sensitive information which is misused

- Vishing – Unknown callers posing as bank representatives and extracting victim’s personal information like PIN or Password to execute fraudulent transactions

- Mone Mule – Fraud rings transfer money to an intermediary account which acts as a money mule to transmit and park money from victims

- SIM Cloning – If a fraudster clones your SIM, he can even change the PIN you use for instant payments

Authorized push payment fraud (APP fraud) where victims are manipulated into making real-time payments to fraudsters, typically by social engineering attacks involving impersonation - Scams when a counterfeit customer asks a seller to click on the “Pay” option to receive payment and thereby source the PIN or OTP necessary to authorise a transaction.

Securing transactions and apps for real-time payments

Banks and other payment processors are used to relying on risk management engines driven by statis rules and leveraging transaction data and bureau scores. However, the current generation payments and lending ecosystem has digital payments at the core of their business. Rules and transaction data are still necessary but not necessarily sufficient to mitigate fraud and risks.

With real-time digital payments accelerating growth, leveraging alternate data and machine learning models are key for instant risk insights to protect against frauds, scams, laundering and delinquency. The same must be complemented by an adequately scalable, low latency and high throughput infrastructure and data pipelines which are possible today.

Alternate data and digital footprints like geolocation, IP, device, and behavioural biometrics (keystroke/mouse dynamics) data provide significant real-time risk insights to secure transactions. It is vital to build this enhanced risk infrastructure in parallel to the instant payments infrastructure to make the best use of the future of payments!

Addressing fraud and risk in real-time payments – now!

As financial institutions gear up to adopt and accelerate their business with real-time payments, it is critical to brace for the risks attached. Learning from scenarios and experience of early adopters in instant payments (like UPI), banks and partners should look at enhancing their risk mitigation infrastructure — and do it now!

Customer change has mirrored evolution in the market. The average user now expects an always-on digital service with as few barriers as possible. This applies whether making regular purchases or significant one-off transactions.

Drona Pay offers a new-age risk management platform which uses supervised & unsupervised machine learning algorithms that leverage device fingerprints, behavioural biometrics, geolocation, app usage patterns and transactional data in real-time to protect instant payment infrastructures for Banks, Card issuers, BNPLs and payment processors.

With an out-of-the-box set of rules and ML models for risk mitigation, easily integrable API-driven infrastructure and a comprehensive case management module, Drona Pay serves as the perfect partner for securing and scaling your real-time payments ecosystem with accelerated go-to-market.

Take the first step on your innovation journey today.